The U.S. insurance industry faces an unprecedented challenge: nuclear verdicts reached $31.3 billion in 2024, a 116% increase from the previous year. Although claim severity is rising about 5 percentage points faster than CPI inflation, yet many insurers are still constrained by legacy IT systems that take months to update pricing and risk models.

This article explores how social inflation is transforming the commercial insurance landscape and why insurers now need greater technological agility. Specifically, we highlight how business rules engines, such as Higson, can help insurers respond quickly to emerging risks and maintain competitive control over pricing and underwriting decisions.

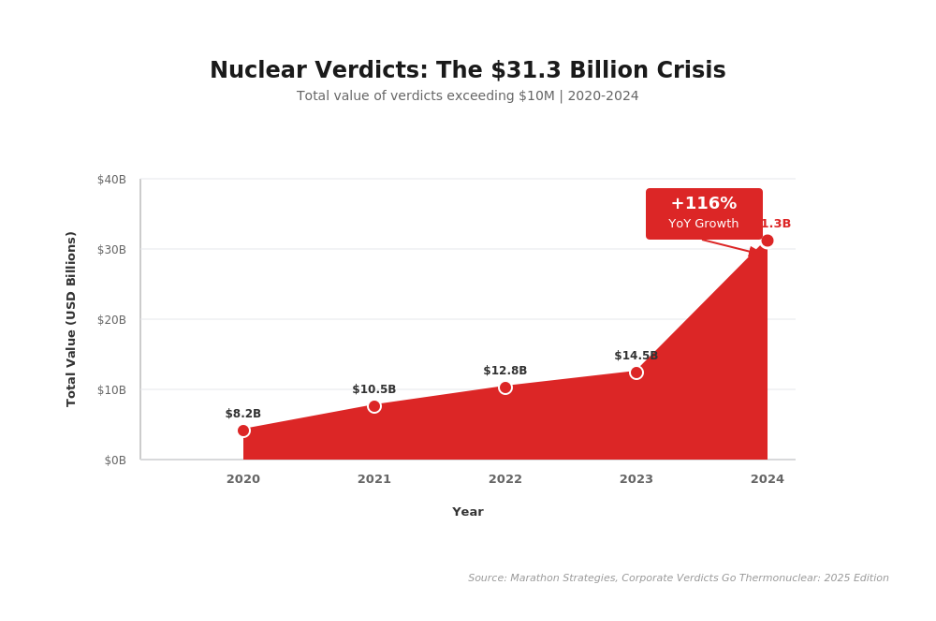

The Breaking Point: 2024 in Numbers

In 2024, insurers faced a stark reality: traditional risk models no longer reflect emerging claim patterns. While CPI inflation remained around 3%, commercial insurance claim severity rose 8%, marking the 14th consecutive year of underwriting losses in Commercial Auto – totaling $4.9 billion (AM Best (2024/2025). U.S. Property/Casualty – Commercial Auto Market Review).

However, rising parts costs and labor rates only tell part of the story. The main pressure comes from social inflation – the persistent rise in claims costs driven by societal, legal, and cultural shifts rather than traditional economic factors.

The Marathon Strategies report reveals the scale of the challenge: nuclear verdicts (awards over $10 million) grew 116% year-over-year, with a median value of $51 million (Marathon Strategies, Corporate Verdicts Go Thermonuclear: 2025 Edition, pp. 10-11).

In an environment where third-party litigation funding (TPLF) has evolved into a $15-31 billion asset class (Westfleet Advisors, 2024, Litigation Finance Market Report), traditional risk assessment methodologies are becoming obsolete. The industry faces a permanent paradigm shift in how personal injury and property claims are litigated and settled.

Understanding Social Inflation: Three Converging Forces

Social inflation is not a linear trend but rather the result of three powerful interrelated forces. They are reshaping the commercial insurance landscape, making traditional risk management methods increasingly inadequate.

1. The Industrialization of Plaintiff Litigation

What was once a system to ensure access to justice has become a highly capitalized industry. Plaintiff law firms now spend over $2.4 billion annually on advertising, creating sophisticated campaigns that actively generate claims. The impact is measurable: nuclear verdicts rose 52% in a single year, and average auto liability verdicts have climbed nearly 50% over the past decade (U.S. Chamber of Commerce ILR, Nuclear Verdicts: Trends, Causes, and Solutions, 2024).

2. Social Media's Influence on Jury Perception

Jurors increasingly arrive in courtrooms influenced by narratives from TikTok, Facebook, and other social media platforms, where corporations are often portrayed as profit-driven entities lacking human consideration. Plaintiff attorneys leverage this by anchoring with extremely high damage requests – $100 million or more – which are becoming more normalized in verdicts (U.S. Chamber of Commerce ILR, 2024).

3. Third-Party Litigation Funding as an Asset Class

Litigation funding has moved well beyond a niche financial tool (with $15-31 billion asset class as we mentioned earlier). With billions in committed capital, these funds enable plaintiff firms to pursue longer, more complex cases, finance extensive discovery, and apply sustained pressure on insurers to settle into early settlements.

Why Insurers Struggle to Respond to Social Inflation

U.S. insurers face a critical paradox: they can see rising loss ratios in real-time, yet their systems prevent them from responding quickly enough.

Many legacy platforms and rigid configurations require extensive coding to update pricing or risk models. Rolling out new rating structures can take months, while social inflation trends can shift in weeks.

Compliance adds another layer of pressure. Regulations such as California’s Proposition 22 (addressing gig economy exposures) and TPLF transparency rules demand rapid adjustments across multiple jurisdictions. Without flexible systems, insurers risk under-reserving or facing regulatory penalties.

In short, this is a crisis of technological agility. Insurers have become hostages to their own data infrastructure - able to observe the problem but unable to execute solutions at the pace the market demands.

The Jurisdictional Mosaic: Why One-Size-Fits-All Pricing Fails

For nationwide commercial insurers, social inflation does not follow a uniform pattern. Instead, it reflects a complex mosaic of state-level legal environments, making one-size-fits-all pricing strategies ineffective and complicating reserve calculations (American Tort Reform Foundation, Judicial Hellholes Report 2024/2025).

Judicial Hellholes vs. Reform States

Underwriters now rely on state-by-state risk maps that highlight dramatic variations in litigation severity:

- High-Risk States: Nevada led in 2024 with $8.5 billion in nuclear verdicts, driven by pro-plaintiff product liability rulings such as the Real Water case. California ranked #3, and New York #5 (Marathon Strategies, 2025; ATRF 2024/2025).

- Reform Success Stories: Florida’s HB 837 (2023) illustrates the impact of legislative intervention. Following tort reform, the state dropped from #2 to #10 in the judicial hellholes ranking.

The takeaway: without the ability to apply jurisdiction-specific pricing and risk selection, exposure in high-severity states can negatively impact the performance of an insurer’s entire portfolio.

The IT Barrier to Micro-Segmentation

Many insurers lack the technical capability to implement rapid, state-specific pricing and risk:

Tariff Inflexibility:

Without a business rules engine, insurers often remain blind to legislative changes until they impact loss ratios. Six-month deployment delays result in systematically underestimated reserves.

Rising Compliance Costs:

Regulations like California’s Proposition 22 require simultaneous updates across multiple jurisdictions. Manual implementation increases costs and extends development cycles, eating into margin.

Discovery Vulnerability:

Third-party litigation funding (TPLF) allows plaintiffs to exploit legacy IT systems, demanding costly document production. Often, paying settlements becomes more economical than litigating, regardless of case merit (Trask, Andrew J. (2024). Third-Party Litigation Funding Justifies Cost-Shifting, Vol. 33 No. 7).

These IT constraints prevent insurers from reacting quickly and precisely, leaving portfolios exposed to social inflation and state-level litigation risk.

2026 Market Outlook: The Two-Speed Reality

Industry forecasts point to a bifurcated market: property lines are stabilizing, while casualty segments face ongoing corrections.

Commercial Auto: The Widening Gap

Underwriting losses exceeding $10 billion across 2024-2025 are driving rate increases of 20-40% for large fleet exposures. Insurers are adopting selective underwriting, sometimes declining monoline auto risks and requiring bundling with workers’ compensation coverage.

Umbrella & Excess: Capacity Constraints

Rate increases of 10-25% are now standard. Reinsurers are limiting capacity due to clash risk, where multiple nuclear verdicts could affect a single catastrophic event or coverage period.

Technology as Competitive Differentiation

Progressive insurers are deploying telematics and predictive analytics with measurable results: 61% reduction in claims costs and 52% fewer accidents (USI Insurance Services, 2026 Commercial P&C Market Outlook). These tools only work when integrated with flexible pricing and underwriting systems.

The Path Forward: Business Rules Engines as Strategic Infrastructure

Social inflation demands that insurers rethink their system architecture. The challenge isn’t just raising rates – it’s having the agility to adjust pricing, underwriting, and risk strategies across jurisdictions, legislative changes, and emerging litigation patterns in days rather than quarters.

This is where business rules engines (BREs) move from being a technical tool – an IT “nice-to-have” – go a strategic enabler. At Decerto, we designed Higson to meet this need: a product configurator and BRE that allows insurers to manage risk dynamically, respond to fragmented legal environments, and update rules without coding.

Use Case: Higson in Action

Consider a commercial insurer with exposure across Nevada and California – two states with dramatically different litigation environments. Here's how Higson enables immediate, precision response:

1. Automated Risk Detection

Higson automatically flags policies in high-severity jurisdictions. Example: Apply a 25% severity surcharge for Nevada commercial auto risks based on current Marathon Strategies and ATRF data feeds.

2. Dynamic Jurisdiction-Specific Pricing

Business rule: "IF jurisdiction = Nevada AND line = Commercial Auto, THEN increase base rate 30% AND restrict Umbrella limits to $5M." Implementation takes hours, not months. No code changes required.

3. Real-Time Litigation Strategy Support

Integrates predictive analytics to model TPLF-backed litigation costs. Provides settle-versus-litigate recommendations based on jurisdiction-specific verdict history and case data.

4. Automated Compliance Adaptation

When regulations change (e.g., California Proposition 22, Florida HB 837), compliance teams update rules through no-code interfaces. Changes propagate instantly across all affected policies.

Conclusion: Turning Complexity into Advantage

Social inflation is transforming the U.S. liability landscape, and insurers can expect it to remain a major driver of risk and cost well into 2026 and beyond. Industrialized plaintiff litigation, social media influence on juries, and sophisticated litigation funding have created a $31.3 billion challenge that traditional insurance infrastructure cannot keep pace with.

The insurers best positioned to thrive will not necessarily have the largest capital reserves or the widest distribution networks. Rather, success will go to those that can observe emerging patterns and execute pricing, underwriting, and claims strategies at market speed.

Business rules engines have evolved from technical tools into strategic imperatives. We built Higson to transform social inflation from an existential threat into an opportunity for competitive differentiation – converting technological agility into sustainable underwriting profit.

The question facing commercial insurers is no longer whether to modernize their rules architecture. It's whether they can do so before the next wave of nuclear verdicts forces the decision.

Take Full Control of Your Product Logic

We provide fee Proof Of Concept, so you can see how Higson can work with your individual business logic.

.png)

.png)

.png)